250,000 Manufacturers. One Story Nobody’s Telling.

TL;DR FAQ: How Mid-Market Manufacturers Are Using Cobots to Compete and Win

▼ Q: What is a mid-market manufacturer and why does this moment matter for them?

A: Mid-market manufacturers are typically companies with 100 to 1,000 employees and $30M to $500M in annual revenue. The sweet spot driving the current automation wave is 200 to 500 employees and $50M to $200M in revenue. This moment matters because three pressures arrived at the same time: a structural labor shortage (433,000 unfilled U.S. manufacturing jobs as of late 2025), margin compression from energy, logistics, and regulatory costs, and global competitors who have already automated. These firms are large enough for automation ROI to be real, but small enough that they have been largely ignored by the media and by most recruiting firms.

▼ Q: Are mid-market manufacturers actually buying cobots, or is this still mostly big-company territory?

A: They are buying. North American robot orders grew 6.6% in 2025, and the growth was led by general industries, not automotive. Collaborative robots hit a record 28.6% share of all robot orders in Q4 2025. Global cobot shipments are projected to reach 125,000 units annually by 2029, a roughly 20% compound annual growth rate. The sectors moving fastest are food processing, plastics and injection molding, metal fabrication and welding, and medical device manufacturing.

▼ Q: What jobs are mid-market manufacturers actually hiring for when they automate?

A: Not Robotics Engineers. The roles in demand are floor-ready and application-focused: Automation Engineers (~$112,000), Controls Engineers ($95,000 to $120,000), Manufacturing Engineers ($85,000 to $105,000), PLC Programmers ($70,000 to $90,000), and Robotics Technicians ($55,000 to $75,000). These are people who can troubleshoot a sensor mid-shift and get a line back up, not researchers. Stackable credentials from programs like the ARM Institute are increasingly more predictive of success than a four-year engineering degree.

▼ Q: How fast is the ROI on a cobot investment for a smaller manufacturer?

A: Faster than most expect. A single-robot palletizing cell typically reaches positive ROI within 6 to 18 months. A $50,000 cobot cell that replaces 1.5 operators per shift can pay for itself in under a year at a $50M manufacturer. Equipment-as-a-Service and Robotics-as-a-Service financing models also reduce upfront capital requirements by 60 to 70%, converting the investment from a capital expenditure to an operating expense, which changes the decision entirely for firms with lean balance sheets.

▼ Q: Which U.S. regions are seeing the fastest mid-market cobot adoption right now?

A: Four regions are leading. The Midwest (Michigan, Ohio, Indiana) is the largest hub, driven by metal fabrication and industrial machinery. The South (Texas, North Carolina, Georgia) is growing fast through reshoring and new facility construction in food, pharma, and medical devices. The Northeast (Massachusetts, New Jersey) is concentrated in life sciences and precision manufacturing. The West (California, Utah) is furthest along in AI-integrated robotics and autonomous mobile robots. Each region has different sector drivers, which affects what roles are in demand locally.

▼ Q: If a mid-market manufacturer can’t build an internal robotics team, what do they do?

A: Most rely on third-party system integrators, especially in the $50M to $100M revenue range. Good integrators identify workflow bottlenecks the internal team is too close to see, connect modern cobots to legacy equipment like older CNCs and ERP systems without a full overhaul, and ensure OSHA and ISO safety compliance for human-robot collaborative environments. The staffing question that follows is: do you hire someone who can manage that integrator relationship effectively, or do you eventually hire to bring the function in-house as you scale? That decision point is underrated and under-discussed.

▼ Q: Is this automation wave actually a threat to manufacturing jobs, or does it create them?

A: Both, but not equally. Cobots are being deployed first in the roles that are hardest to fill and most physically demanding, night shifts, palletizing, repetitive assembly, welding. That frees existing workers for higher-value tasks and reduces turnover driven by injury and fatigue. The jobs being created, Controls Engineers, Automation Engineers, PLC Programmers, pay significantly more than the manual roles they support. The risk is for manufacturers who do not automate: margin erosion and an inability to compete with facilities running 24/7 robotic consistency on basic production tasks.

Every week there’s another piece about a robotics startup raising $200M, or a giant automaker opening a gleaming new smart factory. Great photos. Inspiring CEO quotes. And if you run a 200-person plant in Ohio or Texas or the Carolinas, you read those pieces and none of it applies to you.

You’re not building humanoid robots. You’re building parts. Or packaging food. Or running injection molds around the clock. And you’ve been doing it through a labor shortage, a margin squeeze, and a competitive shift that the business press mostly ignores.

This is for you.

The real picture right now

There are roughly 250,000 manufacturing firms in the U.S. The ones that dominate the headlines represent a tiny fraction of that. The majority are mid-market manufacturers: privately held, regionally rooted, and responsible for a huge portion of American industrial output that nobody seems interested in covering.

The sweet spot is 200 to 500 employees, $50M to $200M in revenue. At that scale, labor costs aren’t a manageable line item anymore. They’re the problem. You’re running multiple production lines, demand is consistent, and you literally can’t find enough people to staff them at full capacity.

Some numbers that should feel familiar:

- 433,000 unfilled manufacturing jobs in the U.S. as of late 2025

- 36,766 robot units ordered in North America in 2025, up 6.6% year over year

- 28.6% of Q4 2025 robot orders were collaborative systems, a record high

That last number matters. It’s not the big automotive plants buying cobots. It’s general industry. Your peers.

Three things hitting at once

The labor crisis is structural, not temporary. The workforce is aging. Factories are often in areas where the labor pool has shrunk. And the jobs hardest to fill are exactly the ones that keep your plant running: night-shift machine operators, packaging line workers, repetitive assembly. The problem compounds. An understaffed line runs at reduced capacity, which limits revenue, which limits what you can pay, which makes hiring harder.

Cobots are the most practical answer most mid-market manufacturers have found, because they’re designed to work alongside people, not replace them entirely. The logic: automate the jobs nobody wants first. The ones causing turnover and injuries. Free your existing people for work that actually requires them.

Your margins are getting squeezed from multiple directions. Mid-market manufacturers typically run 8% to 15% operating margins. Energy costs, logistics volatility, and regulatory compliance are all eating into that. The compliance burden alone is significant: for smaller manufacturers, federal compliance costs can run over $50,000 per employee per year, nearly double the rate for larger firms. You’re big enough to feel that at scale, but not big enough to have a team dedicated to managing it.

One thing manufacturers consistently undercount: the soft costs of manual operations. Overtime, production delays, and the error rate increase that happens when workers are tired at the end of a shift (typically 5 to 10%). A cobot cell eliminates that variance. Output is the same at hour one as it is at hour twelve.

Your competitors have already automated. A decade ago, your main competition was other mid-market domestic firms roughly your size. Now you’re competing against global players who built their automation advantage years ago, using traditional industrial robots that required fenced-off cells, specialized programmers, and multi-million dollar infrastructure.

Cobots change that math. A single-robot palletizing installation can be up and running in two to four weeks and typically hits positive ROI within six to eighteen months. You don’t need to replicate what the big players built. You can get comparable consistency without the capital footprint.

What the recovery looks like

The robotics market had a real correction in 2024. Orders slowed after the post-pandemic surge. But 2025 was a clear rebound, and the composition of it tells the story: growth was led by general industries, not automotive. That’s the mid-market. Food processors, plastics molders, metal fabricators, medical device assemblers.

Global cobot shipments are projected to reach 125,000 units annually by 2029, roughly 20% compound annual growth from 2025. That trajectory reflects one thing: mid-market manufacturers are buying.

Where it’s moving fastest by sector

The sectors adopting fastest share a common trait: tasks that are repetitive, physically demanding, or precision-sensitive in ways that human fatigue disrupts.

| Sector | Primary applications | What’s driving it |

|---|---|---|

| Food and Beverage | Palletizing, packaging inspection, heavy lifting | Injury claims, night shift gaps, hygiene requirements |

| Plastics and Injection Molding | Machine tending, part removal, quality checks | High-mix runs need fast redeployment |

| Metal Fabrication and Welding | MIG welding, material handling | Skilled welder shortage; welding was 22.6% of cobot revenue in 2024 |

| Medical Device | Cleanroom assembly, quality inspection | Regulatory traceability, precision tolerances |

A cheese manufacturer automated its cooling and palletizing process with four robotic cells. Consistent production through weekends, no additional labor. Metal fabricators using cobot MIG welding have reported doubling production speed while cutting labor requirements in half. These aren’t pilot programs. They’re operational.

Where it’s happening geographically

Not evenly. Four regions are moving fastest.

Midwest (Michigan, Ohio, Indiana): The core of it. Once synonymous with automotive, now the leading hub for general industry robotics. Mid-market metal fabricators and machinery manufacturers are buying cobots and articulated robots at a fast pace. Michigan had some of the strongest rebounds in robot orders in the second half of 2025.

South (Texas, North Carolina, Florida, Georgia): Driven by reshoring. Texas leads in electronics and semiconductor automation. North Carolina is a concentration point for medical device and pharmaceutical manufacturing. A lot of these are new or expanded facilities, so automation is being designed in from the start rather than retrofitted.

Northeast (Massachusetts, New Jersey, Philadelphia): High-precision and life sciences manufacturing. The Boston-Cambridge corridor feeds robotics talent into mid-market firms in those sectors. New Jersey remains a significant pharmaceutical and chemical manufacturing base.

West (California, Utah): The software-robotics convergence is most advanced here. AI-integrated cobots and autonomous mobile robots are being deployed in ways that were experimental five years ago.

The hiring mistake some manufacturers make

Mid-market manufacturers are not hiring Robotics Engineers. The title sounds expensive and research-oriented, and the technology has become accessible enough that you don’t need a specialized researcher to deploy and maintain a cobot system. What you need are people who can walk onto your floor, troubleshoot a sensor mid-shift, and get the line back up.

The roles actually in demand:

| Role | What they do | Estimated salary (2025) |

|---|---|---|

| Automation Engineer | Designing and implementing automated workflows | ~$112,000 |

| Controls Engineer | Managing logic, sensors, and electrical systems | $95,000 to $120,000 |

| Manufacturing Engineer | Integrating robots into production goals | $85,000 to $105,000 |

| PLC Programmer | Writing ladder logic for machine communication | $70,000 to $90,000 |

| Robotics Technician | Troubleshooting, calibration, maintenance | $55,000 to $75,000 |

The credentials that matter are shifting too. ARM Institute certifications and similar stackable credentials from industry-aligned training programs are increasingly better predictors of floor performance than a four-year engineering degree. A candidate with hands-on cobot training who can contribute in week two is worth more to most plants than a newly graduated engineer who has never seen a live production line.

Most recruiting firms are running searches built for enterprise tech companies. Wrong titles, wrong credential filters, wrong talent pools. It’s a waste of everyone’s time.

The system integrator piece

Most mid-market manufacturers in the $50M to $100M range can’t build an internal robotics department. That’s not a failure, it’s math. What they rely on instead are system integrators: third-party specialists who bridge the gap between your existing operation and modern automation.

Good integrators do three things most internal teams can’t. They find bottlenecks in your workflow that you’re too close to see. They connect modern cobots to legacy equipment, 20-year-old CNCs, older ERP systems, without requiring a full technology overhaul. And they make sure the installation meets OSHA and ISO safety requirements, which matters when cobots are working next to people.

Knowing how to find people who can work effectively alongside integrators, or eventually bring that function in-house as you scale, is one of the most underrated staffing questions in mid-market manufacturing right now.

The financing shift

Two years ago, upfront capital was the main brake on adoption for manufacturers in your revenue range. That’s changed. Equipment-as-a-Service and Robotics-as-a-Service models can reduce initial capital requirements by 60 to 70%, converting a capital expenditure into an operating expense.

For a manufacturer at $50M to $100M in revenue with a lean balance sheet, that’s not a financing preference. That’s what makes the decision viable at all. You get reduced assembly times, better quality consistency, and higher machine uptime without putting pressure on cash that’s already absorbing cost increases elsewhere.

What’s coming

High-payload cobots (over 10kg) are gaining market share. That means collaborative systems will increasingly handle tasks that currently require traditional industrial robots: engine component assembly, large-format palletizing. AI integration into cobot controllers is reducing the need to explicitly program every scenario, which keeps lowering the expertise barrier.

The end state isn’t a lights-out factory. It’s a facility where your experienced people are doing work that actually requires them, while the robots handle what’s been driving your turnover and workers’ comp claims.

Why STEM Search Group wrote this

We recruit for mid-market manufacturers. We know that your next Automation Engineer won’t show up in a search for “Robotics Engineer.” We know the difference between a Controls Engineer who can thrive in a fast-moving plant environment and one who needs the support structure of a large enterprise. We work in the Midwest, the South, the Northeast, and the West, in the sectors moving fastest right now. If you’re building the team to make automation work, we’d like to talk.

Primary Sources

- https://www.automate.org/robotics/news/robot-orders-grow-6-6-in-2025-as-general-industries-drive-broader-automation-adoption

- https://interactanalysis.com/insight/collaborative-robots-revival-forecast/

- https://www.automate.org/robotics/blogs/cobots-revolutionizing-flexible-manufacturing

- https://marketsandmarkets.com/Market-Reports/collaborative-robot-market-194541294.html

Labor and Workforce

- https://nam.org/mfgdata

- https://www.roboticscareer.org/news-and-events/news/124690

- https://www.bridgeport.edu/news/careers-in-robotics-and-automation/

- https://www.flextrades.com/blog/tag/industry-4-0

- https://www.tealhq.com/job-titles/robotics-engineer

- https://www.online.uc.edu/blog/the-future-of-robotics-and-automation-relies-on-workers-with-advanced-skills

ROI and Business Case

- https://easyrobotics.biz/blogs/how-collaborative-robots-boost-roi

- https://www.techtimes.com/articles/314187/20260121/how-robotics-technology-trends-are-reshaping-automation-robotics-across-every-industry.htm

- https://www.supplychaindive.com/news/warehouse-robotics-adoption-increases-supply-chains/812369

- https://www.mdpi.com/2227-9717/13/3/832

Sector-Specific

- https://www.fortunebusinessinsights.com/food-robotics-market-111974

- https://salasobrien.com/news/food-bev-robotics-for-production-lines/

- https://www.gminsights.com/industry-analysis/collaborative-manufacturing-robots-market

- https://sdgprivatefinance.undp.org/leveraging-capital/sdg-investor-platform/medical-devices-production

- https://www.c3controls.com/white-paper/future-of-robotics-automation-in-manufacturing

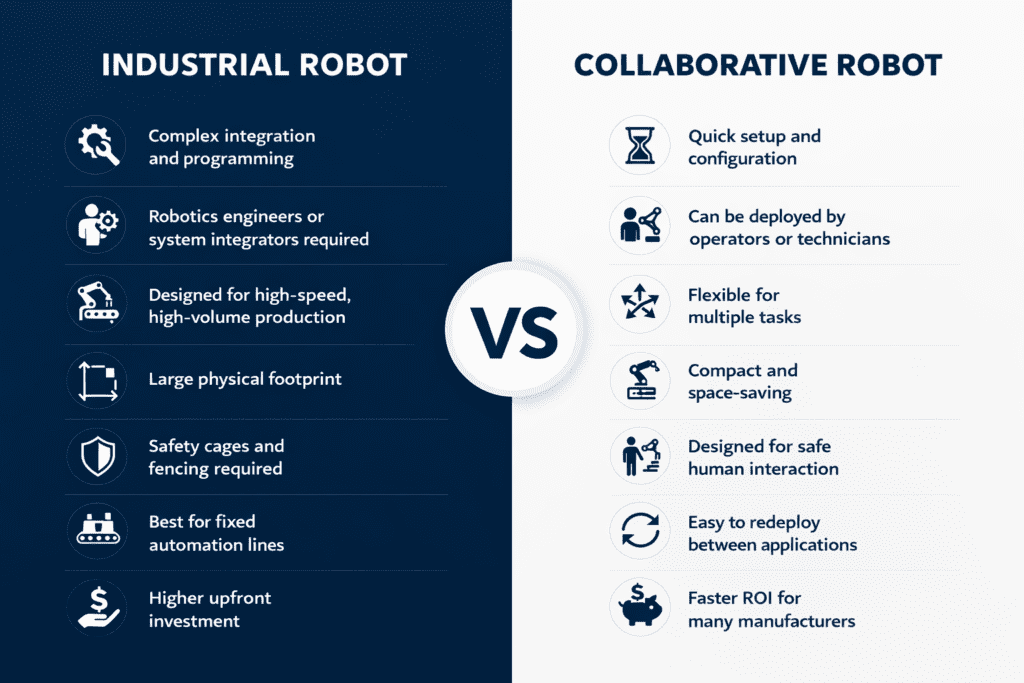

- https://www.iroboticplus.com/blog/Industrial-Robots-vs-Cobots-Which-Is-Right-for-Your-Business_b18020

Regional and Geographic

- https://www.manufacturersalliance.org/research-insights/reshoring-reality-whats-fueling-manufacturing-revival

- https://www.njmep.org/wp-content/uploads/2025/06/2025_IndustryReport.pdf

- https://www.brookings.edu/articles/mapping-the-ai-economy-which-regions-are-ready-for-the-next-technology-leap/

- https://capitalanalyticsassociates.com/mapping-americas-uneven-regional-ai-adoption/

- https://www.imarcgroup.com/united-states-articulated-robot-market

System Integrators